When is the last time your checked your investment allocations? If it has been a few years, a lot has changed in the market. Stocks have reached record highs within the last few months. These gains have probably provided you with a great return. However, they can also set a portfolio’s allocations off-balance.

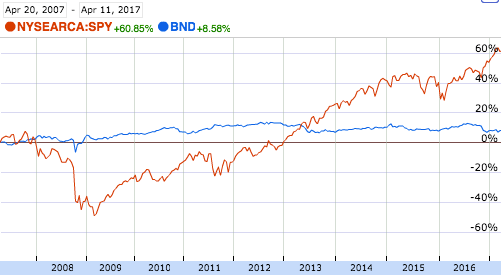

If you invested $10,000 into an allocation of 80% into the S&P 500 (SPY) and 20% into the total bond market (BND) 10 years ago, it would now be worth $15,040, a return of about 50%. Not bad! The price of the stocks went from $8,000 to $12,868. The bonds went from $2,000 to $2,172 . The one problem with this is that the stocks grew faster than the bonds, so your allocation is now 86% stocks to 14% bonds. Your portfolio is now riskier than it was 10 years ago.

Image Source: Google Finance

The 10-year chart for these 2 indexes demonstrates a low correlation coefficient, meaning that the two assets do not have a close positive relationship with each other. In fact, the actual correlation is -0.145. This is good for diversification, but it also shows the importance of reallocating assets as the growth of some assets can set your allocations off balance.

If you would like to keep more of your 50% return from these 2 funds, it is a good idea to rebalance the investment. Rebalancing would move about 6% of the investment from stocks to bonds, returning the portfolio to 80% stocks and 20% bonds. This would reduce your risk back to where you had set it 10 years ago. It also might protect that 6% from losses if a market correction lowers stock prices.

A point of caution: Stocks at an all-time high have historically been more likely to rise than to fall. If this seems counter-intuitive, that is because of the gambler’s fallacy, which leads people to say things like, “what goes up must come down,” or “he hasn’t hit in the last several at-bats, so he’s due.” Just because the market is at an all-time high, does not mean that it is about to go down.

The fact that all-time highs tend to go higher means that it is not necessarily wise to bail out of a bull market. No one can predict how much higher it will go or at what time it will fall. However, a bull market for a particular asset class may throw your portfolio out of balance, making it more or less risky than you had set it up to be (if your portfolio doesn’t automatically rebalance). In other words, it is generally not wise to change allocations just because an asset class is doing well or doing poorly, but it is generally wise to change allocations when they are no longer in line with your risk tolerance.

In future posts, I will cover how you can set up a spreadsheet that automatically updates your current allocations so that you can check them with a few quick clicks. Until then, log in to your retirement and investment accounts and see how they are currently allocated. If you are not sure how a particular fund is allocated, MorningStar is a great resource for looking up specific mutual funds or ETFs. Google Finance is also handy for creating comparison charts like the one I used above.

Disclaimer: This post does not advocate the purchase or sale of particular securities. It simply covers a general strategy for financial allocation.