Like many consumers, my wife and I have long been suspicious of credit card companies. We are generally cautious about debt, not wanting to add to our massive student loan obligations. Credit cards, of course, are among the worst kinds of debt: with high interest rates compounding at a rapid rate.

Up until the end of 2016, the only credit cards we ever had were from making a large retail purchase on credit. For example, I purchased my Macbook Pro with Apple Credit, which is really just a Barclay credit card. The first year has no interest, so I paid off the account in one year and paid no interest. I wanted to keep that line of credit open to build my credit rating, so I set up automatic bill-pay on a bill that is $15/month. I pay off the balance every month, and I don’t use that card for anything else. It has been great for building my credit at no cost. Otherwise, it not very useful and adds to my stress sometimes when I worry about forgetting to pay it.

While teaching my high school personal finance class about credit cards and credit ratings, I decided to do an experiment and try using a cash back card. I compared some cards and decided to apply for the American Express Blue Cash Everyday rewards card. Credit Karma informed me that with my credit history, my application would have a good chance of being accepted, and it was.

While teaching my high school personal finance class about credit cards and credit ratings, I decided to do an experiment and try using a cash back card. I compared some cards and decided to apply for the American Express Blue Cash Everyday rewards card. Credit Karma informed me that with my credit history, my application would have a good chance of being accepted, and it was.

When I filled out my application, I forgot that my credit is frozen. A representative from American Express called me over the phone and was able to quickly bypass the credit freeze and instantly approve my application. He apologized for the inconvenience and sent my card via overnight mail.

I couldn’t help but smirk a bit when I opened the card in the mail a day later. AmEx puts a lot of care into customer service, product packaging, and the look of the card itself, making the customer feel like they are part of an exclusive club as a card owner. An American Express card is more than a revolving line of credit; it really is a membership with special perks. My real reasons for enthusiasm about my AmEx card are the cash back rewards, special discounts, and special protections I get.

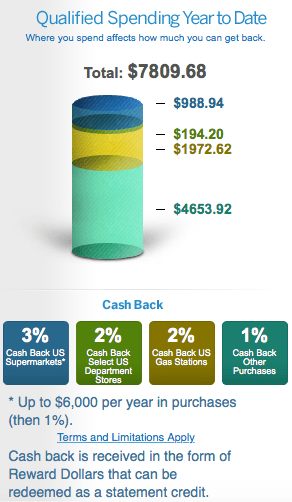

The Blue Cash Rewards program offers 3% cash back at grocery stores, 2% back at gas stations and department stores, and 1% cash back on everything else. I have a long commute and spend about $40/week on gas, so I get about $3.20 in rewards for gas every month.

I pursued cash-back rewards liberally at first because the card had 0% interest for the 1st year. However, I changed my strategy as the year progressed. I had a big dental bill that I was going to need to partially pay with credit, so I used my AmEx card instead of applying for a CareCredit loan. This upped my balance to more than I could pay off at the end of the statement period, so I spent the rest of the year playing catch-up. I got my statement balance back to zero just in time for interest to kick in. That was a huge relief. This showed me how difficult it can be to pay off a revolving line of credit, even with no interest.

Another benefit I found from my card was that it is handy when I have a work expense that I will be reimbursed for. I am usually reimbursed within a week or two, so I am able to pay down my balance without it ever affecting my bank account. I of course get cash back rewards for this, which is really nice when the expense is gas for travel.

The problem with this, however, is one of the fine-print details I overlooked: there is a cap on cash back rewards. Once you have spent $6,000 in a year, all purchases drop to 1% cash back. I probably ignored this because I never thought I would put that much on the card in a year. However, with the dental bill and some work reimbursements, I hit the cap and missed out on the opportunity to earn a few dollars worth of rewards at the end of the year.

The problem with this, however, is one of the fine-print details I overlooked: there is a cap on cash back rewards. Once you have spent $6,000 in a year, all purchases drop to 1% cash back. I probably ignored this because I never thought I would put that much on the card in a year. However, with the dental bill and some work reimbursements, I hit the cap and missed out on the opportunity to earn a few dollars worth of rewards at the end of the year.

There are two other minute details with the reward system that don’t thrill me. One is that I buy most of my groceries at Target, which is not considered a grocery store, so I only get 1% cash back if I spend there (I just use my debit card there instead). The other is that rewards can only be received in $25.00 increments. These small details do not bother me too much, as I don’t want to get too carried away with spending on my card. I don’t ever want to be in a situation where I have to carry over a balance and pay interest on it.

Overall, AmEx does a great job with its rewards program. It is fairly easy to track rewards and to use them. I cashed in $125 in rewards this year.

American Express has excellent security features that help me feel safe using my card. It is extremely easy to login to the web site and track purchases. They email me a weekly account snapshot. They email me when a purchase is made without the card present and when a purchase is made out of state. They also have a feature that will honor product returns when a retailer will not. I have deliberately used my AmEx card in situations where I am worried about the security of the retailer’s payment processing–especially online–or when I am concerned that I might not get what I paid for and have trouble disputing it. For example, I recently used it to purchase a used DVD that I could only find in an online marketplace, just in case the seller didn’t live up to their 4.5-star rating.

American Express takes great care of its customers. I feel a lot less paranoid of credit card companies after using an AmEx card for a year. I also feel less nervous about credit cards because it was easy to keep up with this one. That being said, the real test may be yet to come. Starting with my next statement, I will be charged interest for any balance that I carry over. That makes me a little more nervous. I am not going to stop using the card, but I will not be nearly as liberal as I was in my first several months with it. I will not spend as much on the card in 2018 as I did in 2017, but I am a satisfied AmEx customer and will probably keep taking advantage of their perks for a long time!

Disclosure: I have no relationship with American Express. This is purely a customer review.