You know that you need to budget, save, and pay off debt. Your parents, your teachers, your friend who is a financial advisor, and the morning news show you watch have all told you so. You made a list of bills and expenses and subtracted them from your income, figured out how much you had left, and maybe put some of that into your savings account every month. You’ve been doing that for awhile and don’t seem to be getting anywhere. The savings always gets spent, or somehow the money never makes it into savings in the first place. Something always comes up. The student loan debt seems like it is never going to go away, and saving up to buy a house is never going to happen. It’s time to look at a new approach to budgeting.

I have already written here about calculating your net worth and using that to set goals. I call that being in “the net worth mindset.” Part of the net worth mindset is budgeting based on improving your net worth. This is something I try to teach my students and have personally been working to improve.

My wife and I reevaluate our budget every December and see what we can improve for the next year. This year we split it into categories: income, household bills, debt, savings, discretionary. Subdividing it lets us look at what we are spending on each category. We got more specific about our discretionary spending allocations, and we determined that we could put more money into the debt and saving categories. Household bills, including rent and utilities, only make up 25% of our spending. If we were only making minimum payments, debt would make up 29%.

Paying Off Student Loans Faster without Increasing Income

We decided in 2017 to devote less money to saving and investing and more to paying off debt, especially since the interest rates on my private student loans kept increasing and were getting ridiculous (see this story about what Navient is doing to borrowers). We started paying extra on the principal of those loans and snowballing payments. The extra $200 per month has made a huge difference, but we wanted to distance ourselves from Navient even faster. We had to squeeze more money out of the budget to do it.

The key, I decided, was to get more specific about the budget. We had previously budgeted what we needed, added a little extra allocation for savings or debt, and used what was left as discretionary spending. When variable expenses increased, we just cut back discretionary spending. This worked okay, but it allowed for some waste. We felt like we could make more room for paying off extra debt. We would have to be more detailed to find more money.

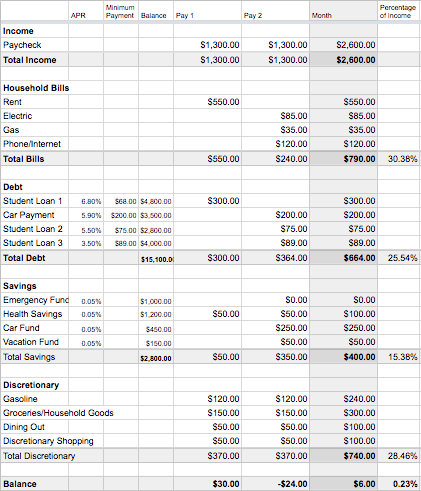

For years, we have budgeted $200 per month for health care expenses. We do not spend that much every month, but we save it. It seems like at least once a year we have something come up that costs hundreds of dollars, such as dental fillings or a hospital visit. Since we have saved $200 per month leading up to that, we are almost always ready to cover it. Now that I am on an HSA plan, that money is automatically deposited into my HSA, $100 from every paycheck.

We decided to apply this same approach to our auto expenses. We established a more specific car expense allocation in our budget. It accounts for car washes and oil changes and saves extra money for long-term maintenance and repairs, similar to how our HSA allocation allows for monthly chiropractor visits and saves extra for annual check-ups, semi-annual specialist appointments, and emergencies. Like we do with the HSA, we will now put $250 into the car fund. We might spend $75 of that on 2 car washes and an oil change and save the other $175. Months later, we will have hundreds of dollars available to cover a repair or to make the next car insurance payment.

We also got more specific about discretionary spending so that we are not eating out or making extra purchases more often than we should. We now have a specific category for that kind of spending and a cap for now much we will spend.

This allowed us to increase our allocation for paying off debt from 29% to 38% of our budget. By picking up the pace, we will have most of our debt paid off within 2 years. This will get us on track toward are goal of buying a house after I finish graduate school.

Net Worth Budget Example

Here is an example of the way we set up our new budget. I created this sample budget based on a single adult who rents and has student loan debt:

You can see that I included the APR, minimum payment, and balance for each account to help manage deciding which to pay extra on first.

You can also see that I included Pay 1 and Pay 2 columns. My wife and I found that most of our bills were due at the beginning of the month, then we had extra money in the middle of the month that we had to remember not to spend. That was too easy to mess up, so a few years ago we decided to split our monthly budget into 2 columns and pay some of our early-month bills 2 weeks early with our late-month bills to avoid this.

2 Important Rules for Paying Extra on Student Loans

1. Emergency Fund First

Notice that in the above budget, $0 per month is assigned to the emergency fund. I agree with Dave Ramsey’s policy of establishing a $1,000 emergency fund before making extra payments on debt. If the funds are withdrawn for an emergency, then this individual should go back to the minimum payment of $68 on Student Loan 1 and put $232 per month into the emergency fund until it is back up to $1,000 before resuming extra payments on Student Loan 1.

2. Confirm That Extra Payments Apply to Principal

Another way that Navient tricks borrowers is to not properly apply their extra payments. You pay extra on your loan, and you notice that the next month your required minimum payment is lower. This must be because the principal balance went down, right? Wrong! It is because they apply the extra payment to the following month by default. It did not go to the principal owed on the loan.

I had to dig around Navient’s web site and find a special tool for making an extra payment. There, I was able to specify which loan it would go to and whether or not it would apply to the principal or the following loan’s balance.

Conclusion

I am done with Navient’s trickery! I am squeezing every penny out of my budget and using almost all bonus pay and side hustle pay to go nuclear on my Navient loans so that I never have to work with this disgusting, abominable corporation ever again. $1,000 or more per month until those balances are all at $0!

My budget can most certainly be better than it is. That is why I revisit it and improve it every year. Each year, it gets more detailed than it was the year before. The less ambiguity you have in your budget, the more effective you can be at eliminating waste. Your hard-earned pay should go toward the things that matter most to you. Your spending should be aligned with personal goals based on your personal values. Thinking in the net worth mindset and getting more specific about how you budget can give you the financial muscle you need to achieve your goals.

I agree completely with you on the emergency fund strategy. We followed Dave’s idea and now have 3 months of emergency funds. We never had so much cash reserve our entire life!! I love the net worth mindset as it makes me prioritize my spending and focus on building wealth.

LikeLike